For most of Bitcoin's history, investors evaluated it the same way they evaluated equities: by watching the price. That framework is beginning to change at the institutional level, and the change has a direct implication for how managed Bitcoin mining exposure should be evaluated. In May 2026, the Schwab Centre for Financial Research published a paper arguing that mining production costs, the measurable, recurring expenditure of electricity, hardware, and infrastructure required to produce each Bitcoin, is now the primary lens through which they value the asset.

The paper, authored by Jim Ferraioli, Director of Digital Currencies Research at Charles Schwab, draws a direct parallel to how commodity analysts have long valued gold, oil, and copper: by the relationship between market price and the cost of bringing new supply into existence.

How Production Cost Becomes a Valuation Anchor

The commodity analogy is instructive. An oil producer with a breakeven cost of $40 per barrel is structurally resilient when oil trades at $60. An oil producer with a breakeven of $70 is under pressure at the same price. The market price matters, but the cost structure determines which producers survive a downturn and which do not.

Bitcoin mining operates on the same logic. Schwab's research identifies two relevant cost benchmarks as of May 2026: efficient miners carrying a production cost of approximately $60,000 per BTC, and inefficient miners carrying a production cost of approximately $95,000 per BTC, based on Glassnode data. The zone between those two numbers defines where Bitcoin's valuation is currently anchored in Schwab's model, and it defines the margin pressure experienced by operations at each end of the spectrum.

The Self-Regulating Mechanism That Makes This Framework Meaningful

What makes the production cost framework applicable to Bitcoin specifically is the difficulty adjustment. Every two weeks, the Bitcoin protocol recalibrates the computational target for block production to maintain a steady output of one block every ten minutes. When hashrate (the total computing power on the network) rises, difficulty increases, and production cost rises. When hashrate falls, because unprofitable miners have curtailed operations, difficulty decreases, and production cost for remaining miners falls.

This mechanism means production cost is a dynamic benchmark that adjusts in response to miner behaviour, which in turn responds to price. When Bitcoin trades below the production cost of inefficient miners, those miners reduce or pause operations. Hashrate declines and difficulty adjusts downward over the following two-week window. The block reward remains fixed at 3.125 BTC every ten minutes, regardless of how many miners are active, but selling pressure on the market decreases because fewer unprofitable miners are forced to liquidate newly mined coins to cover their operating costs. Supply pressure fades as a result, and the conditions for price recovery build through the same self-correcting economic dynamic built into Bitcoin's protocol that has operated without interruption since 2009.

What Efficient vs Inefficient Actually Means in Practice

The $35,000 gap between efficient and inefficient production costs in Schwab's framework reflects the concrete operational differences between mining infrastructure built on fixed, low-cost energy and mining infrastructure exposed to market electricity rates. An efficient miner producing at approximately $60,000 per BTC has secured long-term energy contracts or owns generation assets, operates hardware at or near its thermal efficiency limit, and runs in a jurisdiction where grid costs are structurally low. A hydropower concession in Norway with a fixed tariff for ten years, or a solar facility in the UAE with a levelised cost of energy that does not move with fuel prices, are examples of cost structures that do not deteriorate as hashprice declines.

An inefficient miner producing at approximately $95,000 per BTC is typically operating older hardware at higher electricity rates, purchasing power at market prices in jurisdictions where energy costs fluctuate with demand, and carrying a cost structure with limited downside protection when Bitcoin price and hashprice move against it simultaneously.

For investors evaluating managed mining exposure, the Schwab framework makes the cost structure question unavoidable. The question is no longer simply "will Bitcoin go up?" It is "does the operation I am invested in sit at the $60,000 end of the production cost band, or closer to the $95,000 end?" The answer determines whether the investment performs through a full cycle or faces the margin compression that characterises the inefficient producer cohort.

Related: Why Energy Contracts Matter More Than Hashrate in Bitcoin Mining

Revenue Diversification as a Cost Structure Advantage

Ferraioli's paper makes a second argument that reinforces the managed mining thesis. Bitcoin miners diversifying into AI high-performance computing infrastructure do not weaken Bitcoin's network security. They strengthen miner resilience by reducing dependence on Bitcoin price as the sole revenue driver. When a mining operation generates revenue from demand response participation (agreements where miners reduce energy consumption during peak grid demand in exchange for payment), heat recycling, or AI compute hosting during off-peak power hours, it reduces the forced selling pressure that miners under margin stress typically apply to the Bitcoin market.

Operations with multiple revenue streams carry a lower effective production cost on a Bitcoin-equivalent basis, because ancillary revenue offsets the fixed costs that would otherwise be covered by selling mined Bitcoin at whatever the spot price happens to be. The Schwab analysis provides institutional validation for an operational model that infrastructure-grade managed mining has been building toward for several years.

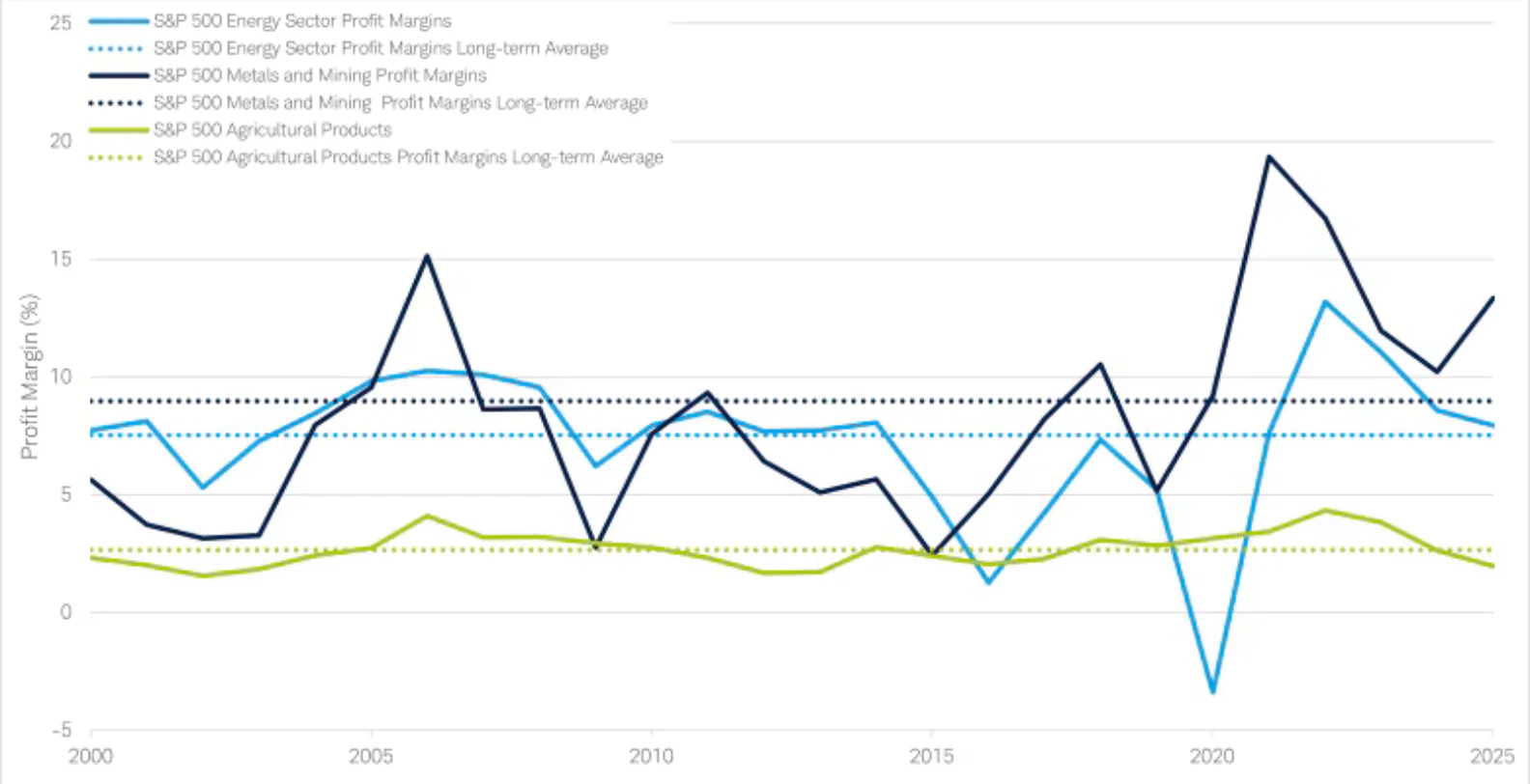

Figure 1: Commodity producer profit margins, energy, metals, and agriculture versus Bitcoin miners (Schwab, May 26, 2026)

Figure 1: Commodity producer profit margins, energy, metals, and agriculture versus Bitcoin miners (Schwab, May 26, 2026)

This chart, published in Schwab's research, shows that commodity producers across energy, metals, and agriculture have historically operated on single-digit profit margins. It positions Bitcoin miners as a recognisable category within that universe, reinforcing the argument that production cost methodology is the appropriate valuation lens for the asset class.

The Institutional Framework and What It Changes

The most important signal in Schwab's paper is the category it places Bitcoin in. An asset valued through production cost methodology is an asset that institutional analysts, portfolio managers, and wealth advisers can place inside a commodity allocation framework. It can be stress-tested against energy cost scenarios, benchmarked against other commodity producers, and evaluated using the same tools applied to gold, oil, and copper for decades.

That analytical familiarity lowers the barrier to institutional allocation. When Schwab tells its advisers managing more than $5.3 trillion in client assets to value Bitcoin through mining metrics, those advisers have a framework for the conversation that did not exist two years ago. The questions institutional capital is now trained to ask, what is the energy cost, what is the production cost benchmark, where does this operation sit in the efficiency range, are precisely the questions that well-structured, infrastructure-grade managed mining is built to answer transparently.

Related: Capital Efficiency in Bitcoin Mining

What This Means for Investors Evaluating Bitcoin Mining Exposure

Schwab's framework gives investors a structured way to assess Bitcoin's risk-reward at different price levels, and a structured way to assess the quality of mining exposure at those same price levels. At current prices within the $60,000 to $95,000 production cost band, the operations that remain viable are those with the lowest and most stable cost structures: fixed long-term energy agreements, efficient hardware, transparent operating terms, and locations with access to low-cost renewable power.

Operations with long-term power purchase agreements in low-cost renewable jurisdictions sit at the most resilient position within the cost band. For investors, the Schwab analysis is a framework for evaluating which mining operations are structurally positioned to produce Bitcoin through the next cycle, not just which ones are running today.